| Newton-Evans recently completed our annual survey

of suppliers of equipment, systems and services to the utility

industry. The results of the survey, which involved more than

25 senior industry marketing and business planning executives

from around the world, reveals supplier perspectives for

automation (primarily T&D) spending by utilities. Why, you

might ask, are the concerns of T&D suppliers important to

you, working in the T&D field at a utility in North

America or Europe or Asia?

Well, first of all,

these observations parallel closely the issues raised by

utility executives in our most recent utility surveys. Most

importantly, uncertainty over deregulation (and/or

privatization) is a reality in today's utility work place in

many areas of the world. Uncertainty breeds inaction,

hesitancy to purchase T&D equipment, systems and services

except on a "must have" basis to serve load growth. Management

decisions regarding T&D automation are most often made on

the basis of knowledge about current and near-term to mid-term

operating environments.

In addition, when

management questions future T&D asset ownership, operation

and maintenance of field (and automation) assets, and finds

answers unavailable, it is unlikely that procurements will be

authorized. The deregulation concerns that are on the minds of

workers at utilities are also on the minds of suppliers.

Survey respondents were asked to rank nine issues as either

"critical," "somewhat important" or "not important" as related

to their T&D automation business outlook. The top concern

was "uncertainty over deregulation and/or privatization." This

concern seemed important to suppliers regardless of where they

were located.

"Thinning profit

margins" was the next highest concern of the respondents.

Eroding profit margins (or increasing operation losses) are

not only issues facing T&D equipment and system suppliers

but are a real possibility facing your own utility in the

not-so-distant future. If there is not much profit potential

in developing, manufacturing, or servicing the T&D systems

and equipment marketplace, suppliers will be forced to turn

their attention and R&D investment funds to other, more

promising, markets and may simply close up shop.

Two issues vied for

third place: the Asian financial crisis (at least for

companies with automation business interests in that region of

the world) and the rapid pace of technological innovation.

Even remote events such as the current Asian financial crisis

are likely to have an effect on your T&D planning, product

pricing and product availability. Regional crises may further

erode the supplier potential for profitable operations. Giants

such as General Electric, Siemens and ABB may have to rethink

their product and marketing strategies, T&D equipment and

systems development schedules and factory loading. They may

have to conduct other business risk assessments when major

events such as this monetary and financial crisis occur. In

turn, such events often result in a direct and dramatic shift

in your options.

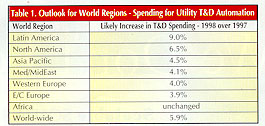

The industry

business executives surveyed were also asked to provide their

estimates of market direction and degree for 1998. While the

forecast was positive overall—looking for worldwide growth on

the order of 6%--some regions look more promising than others

(Table 1). Latin America spending will likely increase the

most with North America and Asia Pacific following.

In summary, two

observations should be made. First, the suppliers seem to have

a more optimistic outlook on spending plans than the utility

managers recently surveyed, at least in North America.

Secondly, it is still dangerous to group transmission and

distribution spending plans together because they are most

often on different paths. While transmission automation

spending may remain conservative a while longer, distribution

spending should increase more rapidly.

The chart above is

based on January 1998 surveys of 25 industry executives from

companies located in North America, Europe, Latin America, and

Asia Pacific.

|