Excerpts from the Newton-Evans’ 2024-2026 Market Overview Series

The 2024-2026 edition of Market Overview for HV Equipment includes 15 topical reports on modern high voltage and transmission-related equipment and systems. This month’s article presents some highlights from four of these market overview reports. In May and June, we provided a total of 14 summaries of modern substation components. Earlier this year, we provided articles on power and distribution transformers. Read the articles below today’s lead article for descriptions of the substation automation/digitalization market and for transformers.

First, lets take a look at what NERC’s year-end 2024 tabulations of transmission projects reveals in the accompanying three charts.

Here is a view (courtesy of STATISTA) of annual transmission capacity additions completed in the United States through 2024, that add to the total market opportunity for FACTS.

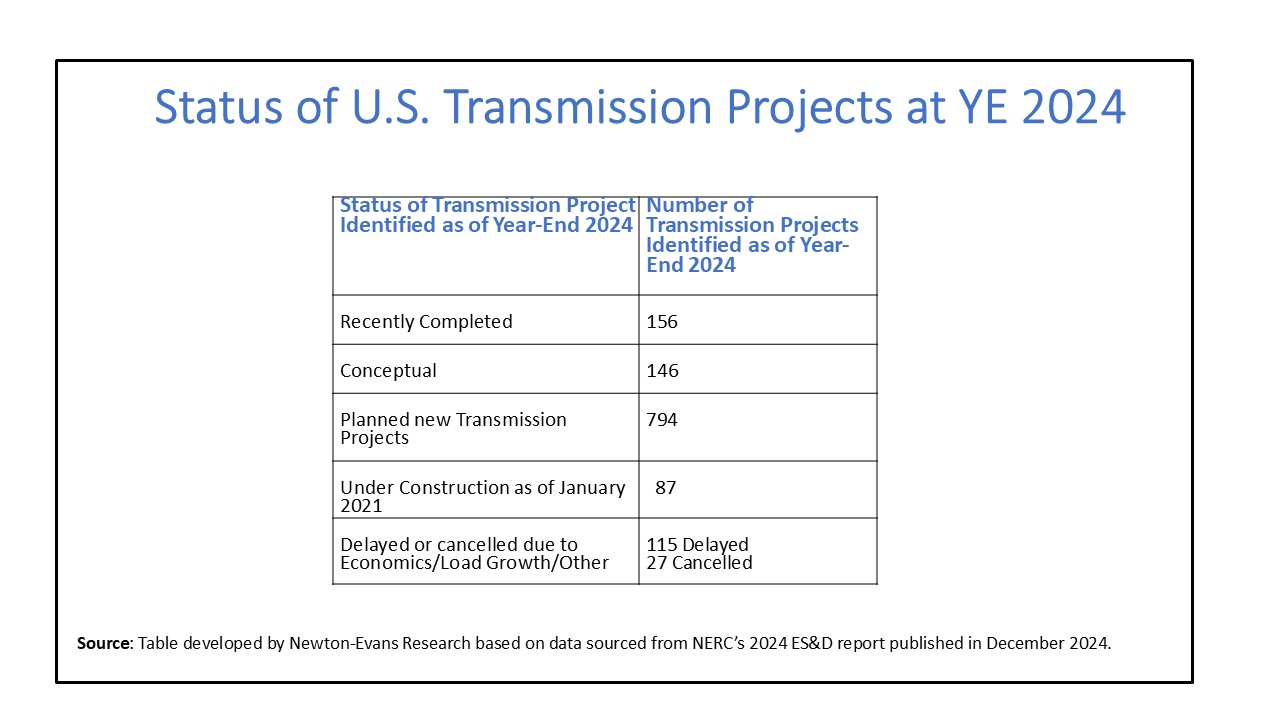

Next is a table developed by Newton-Evans Research indicating the status of 1,325 transmission projects from across the United States, as identified by NERC as of year-end 2024.

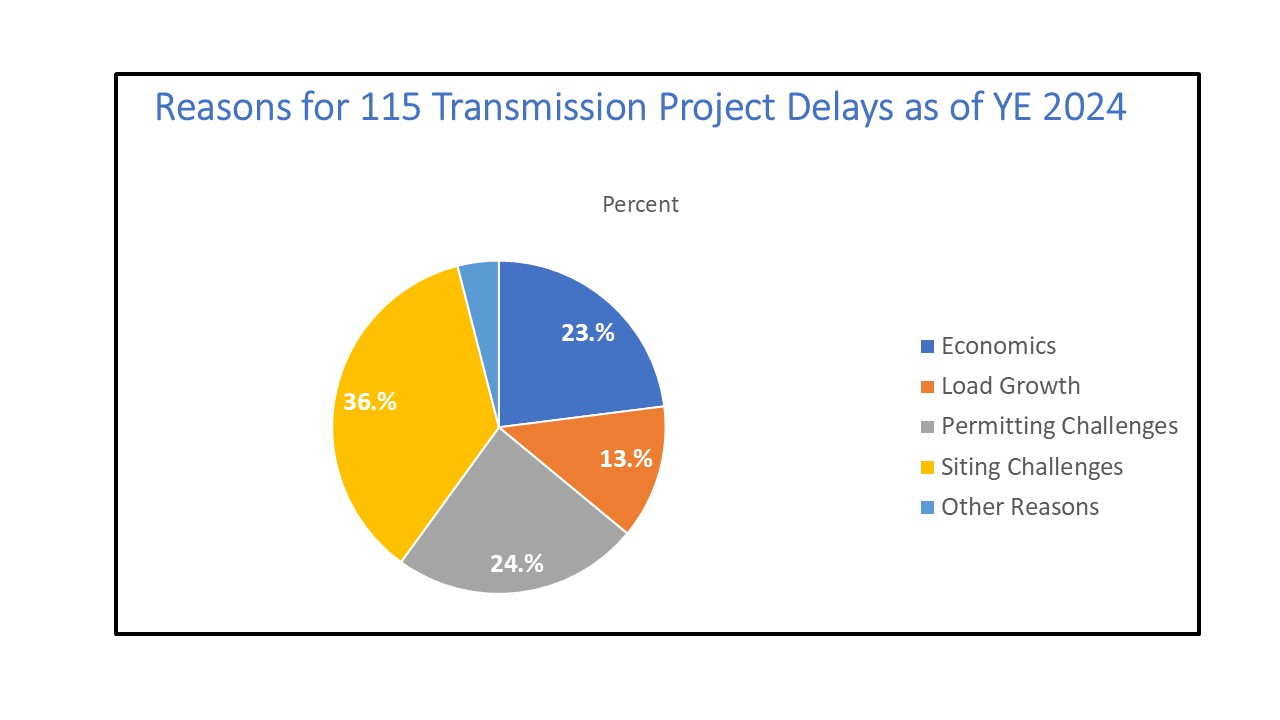

The third chart is provided to indicate the reasons given for project delays in transmission construction programs as of year-end 2024. This chart was also sourced from data provided in NERC’s 2024 Electricity and Supply report file.

Information from the NERC and related DOE files, along with utility surveys and supplier discussions are the basis for information provided in the entire 15-report series of high voltage equipment and power transmission system components prepared by Newton-Evans. Details and ordering information can be found here: https://www.newton-evans.com/product/overview-of-the-2024-2026-u-s-transmission-and-distribution-equipment-market-high-voltage-series/ . The complete 2024-2026 series is priced at $1,450.00, with individual 3–5-page report summaries available for $195 per market overview. Each report provides product/system/component definitions, revenue estimates of key suppliers, overall market segment size, market share assessments, outlook through 2026, and revenue split between sales to utilities and commercial-industrial buyers.

Detailed information including shipment estimates, key market participants and market trends are included in the actual market overviews. We will provide highlights of additional HV equipment types for our website visitors within a few weeks. Following are the HV equipment/system topics for this month:

FACTS: A Flexible Alternating Current Transmission System (FACTS) is a system composed of static equipment used for the AC transmission of electrical energy. It is meant to enhance controllability and increase power transfer capability of the network. It is generally a power electronics-based system. According to GE Vernova, FACTS provides the ability to deliver reactive power support, enhance controllability, improve stability and increase power transfer capability of AC transmission systems.

IEEE definition for FACTS: “a power electronic based system and other static equipment that provide control of one or more AC transmission system parameters to enhance controllability and increase power transfer capability.”

Siemens Energy indicates that FACTS improves transmission quality and efficiency of power transmission by supplying inductive or reactive power to the grid. According to Hitachi Energy, FACTS consists of three technology branches: series compensation, dynamic shunt compensation, and dynamic energy storage. The most common form of leading reactive power compensation (RPC) is by connecting shunt capacitors to the line.

Major categories of FACTS offerings include the following:

Fixed Series Compensation (FSC), Static Compensation (STATCOM), Static Frequency Converters (SFC), Static VAR Compensation (SVC), and Thyristor Controlled Series Compensation (TCSC)

In one recent Newton-Evans study, the following information was developed from survey information gathered from about 30 power generation/transmission facilities.

• Usage of FACTS: Requested information on whether or not the respondent was using any FACTS devices. Forty percent of participants reported some use of FACTS.

• FACTS devices in use: For FACTS user sites, respondents were requested to indicate which FACTS devices/approaches were being used. SVC was in use at 75% of FACTS sites, while STATCOM was reported as in use by about 60% of the sub-group of FACTS users.

One 2024 CAISO report listed the estimated cost for an SVC unit at $20-30 million for an EHV project in California.

Separately, a precursor form of FACTS can be found in the ongoing usage of older synchronous condenser technology. In addition to the FACTS market sizing estimates shown in the FACTS market overview report, synchronous condenser sales estimates in the U.S. are also provided. Condensers are treated separately as the drivers for that technology is found in large fossil plant shutdowns, erosion of spinning reserves, lack of grid forming devices, as well as in use to counter the impact of renewables on grid stability.

Leading supplier of FACTS and RPC in the United States include HITACHI ENERGY, GE VERNOVA, SIEMENS ENERGY AND MEPPI.HVDC System: A High Voltage, Direct Current (HVDC) electric power transmission system uses direct current for the bulk transmission of electrical power, in contrast with the more common alternating current systems. For long-distance transmission, HVDC systems may be less expensive and suffer lower electrical losses. For underwater power cables, HVDC avoids the heavy currents required to charge and discharge the cable capacitance each cycle. Two main cost components are the converter stations and the cable.

The Brattle Group has prepared an excellent guide and tutorial, “The Operational and Market Benefits of HVDC to System Operators.” This guide is available to download courtesy of the American Council on Renewable Energy (ACORE) at https://acore.org/wp-content/uploads/2023/09/The-Operational-and-Market-Benefits-of-HVDC-to-System-Operators.pdf

Normally manufacturers such as those identified above do not state specific cost information of a particular project since this is a commercial matter between the manufacturer and the client, which, in the case of HVDC projects, is usually a non-utility corporation/LLC that is set up specifically for managing the HVDC project.

HVDC project costs vary widely depending on the specifics of the project such as power rating, circuit length, overhead vs. underground/underwater route, land costs, and AC network improvements required at either terminal. A detailed evaluation of DC vs. AC cost may be required where there is no clear technical advantage to DC alone and only economics drives the selection.

Typically, the longer the transmission route, the more cost-effective can be HVDC.

There are a handful of HVDC U.S.-based projects either about to get underway or planned for construction during 2025-2026. Several more remain on the drawing board awaiting the required routing approvals and funding from multiple parties. Each project we have found is estimated to cost well over one billion dollars. Only a portion of that total project cost will be awarded to one of more of the above-listed firms for HVDC converter stations. However, each award to the above suppliers will be worth multiple millions of dollars.

Since the earlier 2021-2023 edition of this report, three projects have been cancelled/postponed indefinitely. These include Plains and Eastern Clean Energy Link; Rock Island Clean Line and Juan de Fuca Cable HVDC. The current U.S. HVDC projects underway, about to begin, or still in the pipeline of possibilities includes a total of eight named projects that Newton-Evans has uncovered. Together, these announced projects are valued at around $50 billion level of investment. Hitachi Energy, Siemens Energy and GE Vernova are the key suppliers of HVDC in the U.S.

Air-Insulated Substations: There are three categories of Air insulated (AI) Substation EPC providers. These include: (1) the HV and MV equipment manufacturers offering EPC services, (2) Top tier EPC firms, and (3) second tier EPC firms. These EPC firms provide total “turn-key” substation design, engineering and construction services. When manufacturers are awarded AI substation awards, they most often will utilize their own equipment wherever plausible. EPC firms tend to specify and integrate substation equipment from multiple suppliers. Tier One EPC firms typically construct large HV substations while Tier Two and smaller EPC firms specialized in MV substations. Internationally, large HV/MV equipment manufacturers account for a higher share of turn-key EPC activities for greenfield substation projects than they do in North America. A more recent addition to the global need for small substation construction for mid-size renewables operations has meant an increase in the number of available substation construction firms able and willing to work in remote areas of the United States.

Based on NERC projections, there are plans to add about 18,675 miles of HV transmission lines over the 2021-2030 decade. All of this expansion will be at 100kV or higher. This in turn impacts substation design and build costs. Nearly 300 transmission substations will be constructed (or uprated) to accommodate these new line additions.

Source: https://www.nerc.com/pa/RAPA/ra/Reliability%20Assessments%20DL/NERC_LTRA_2023.pdf

Costs for AIS substation engineering, procurement and construction activities are unique to each substation project. In the U.S. market, our estimates range from a low of $7-10 million for some MV substations – and even a bit lower for construction of smaller substations at remote renewable sites, to a high of more than $80-200 million for HV/EHV substations. UHV substations, already in progress internationally, may cost upwards of $500 million.

IOUs, G&Ts and Federal Sites are most closely identified with HV substation construction plans, while distribution cooperatives, municipal and other public power operations and industrial sites indicated primary involvement with MV substation construction plans. Merchant plants for this report are most often associated with construction of MV substations for renewables farm/park sites.

Reliability and congestion relief have been cited by NERC as the two principal drivers for new transmission line construction. Siting and permitting are the two obstacles that continue to plague more rapid development of transmission capacity.

A Gas Insulated Substation (GIS) is an electric power substation in which all live equipment and busbars are housed in grounded metal enclosures sealed and filled with sulfur hexafluoride gas. Also defined by the U.S. DOE as an integrally constructed substation in which all the apparatus units (circuit breakers, disconnect switches, current and voltage transformers, and surge arresters) are isolated from air in metal tanks filled with sulfur hexafluoride (SF-6) gas.

EPC firms play a key role in the HV GIS substation market as the majority of GIS-using utilities continue to outsource engineering, procurement and construction activities to EPC firms or to the EPC subsidiaries of large GIS manufacturers.

We have defined three categories of gas insulated substation EPC providers. These include (1) the HV and MV GI equipment manufacturers offering EPC services, (2) Top tier EPC firms, and (3) second tier EPC firms. These firms provide total “turn-key” substation design, engineering and construction services. When manufacturers are awarded GIS substation awards, they most often will utilize their own equipment wherever plausible (e.g., Siemens EPC contract for large HV GIS substations are with State of New Jersey). Tier One and Tier Two EPC firms tend to specify and utilize substation equipment from multiple suppliers. Tier One EPC firms typically construct large HV GIS substations while Tier Two and smaller EPC firms specialize in MV GIS substations. Internationally, large HV/MV equipment manufacturers account for a higher share of turn-key EPC activities for greenfield substation projects- both GIS and AIS types.

More than one-half of the respondents (55%) in a recent Newton-Evans’ study indicated they were considering turnkey approaches for civil and construction work, while major equipment would be furnished by the company through separate supplier agreements. Forty-two percent were considering full or partially engineered packages from EPCs and 29% directly from suppliers. Nearly one-third of the respondents were considering complete turn-key approaches for at least one or more projects.

Sources: Newton-Evans Research Company (HV GIS construction site visits and meetings with multiple GIS-related EPCs), along with data on BPA, Siemens, Hitachi Energy, HICO websites.

Observed turnkey prices for U.S. gas insulated substations over the past few years have ranged from $8 Million to $125 Million among the few publicized awards that have been publicly disclosed indicating a project price.

The estimated total 2023 expenditures for EPC-related work (except for gas-insulated switchgear) and outlook through 2026 is provided in the market overview.

The total U.S. market value of all substation construction activities for both greenfield and brownfield projects was likely approaching $n Billion in 2023 in “hard dollar” expenditures (for siting, construction, equipment costs) by electric utilities and industrial/commercial firms. As utilities around the world increasingly adopt a “green” attitude toward the environment, there has been a desire for non-SF6 alternatives to GIS developments. Up until about 2020, the highest voltage level non-sf6 GIS switchgear was about 145kV. By year-end 2025, we believe almost all HV and EHV voltage ranges will be available. Complete GIS configurations that will successfully operate with either non-SF6 gas mixtures or use clean air/vacuum technology for HV breakers will be offered by major GIS market participants.

summary reviews and highlights from completed studies

summary reviews and highlights from completed studies