The medium voltage equipment market in the U.S. is comprised of multiple types of equipment both large and small, some getting more expensive per unit while others have tended to remain available at a relatively stable price range over the past few years. The 2026-2028 edition of the Medium Voltage Equipment series of Market Overviews will be available in mid-July. This article provides some of the highlights from the upcoming series.

There are some segments of the MV equipment market that have now crossed the billion-dollar threshold and others have climbed into the hundreds of millions over the past three years, comprising the post-COVID era.

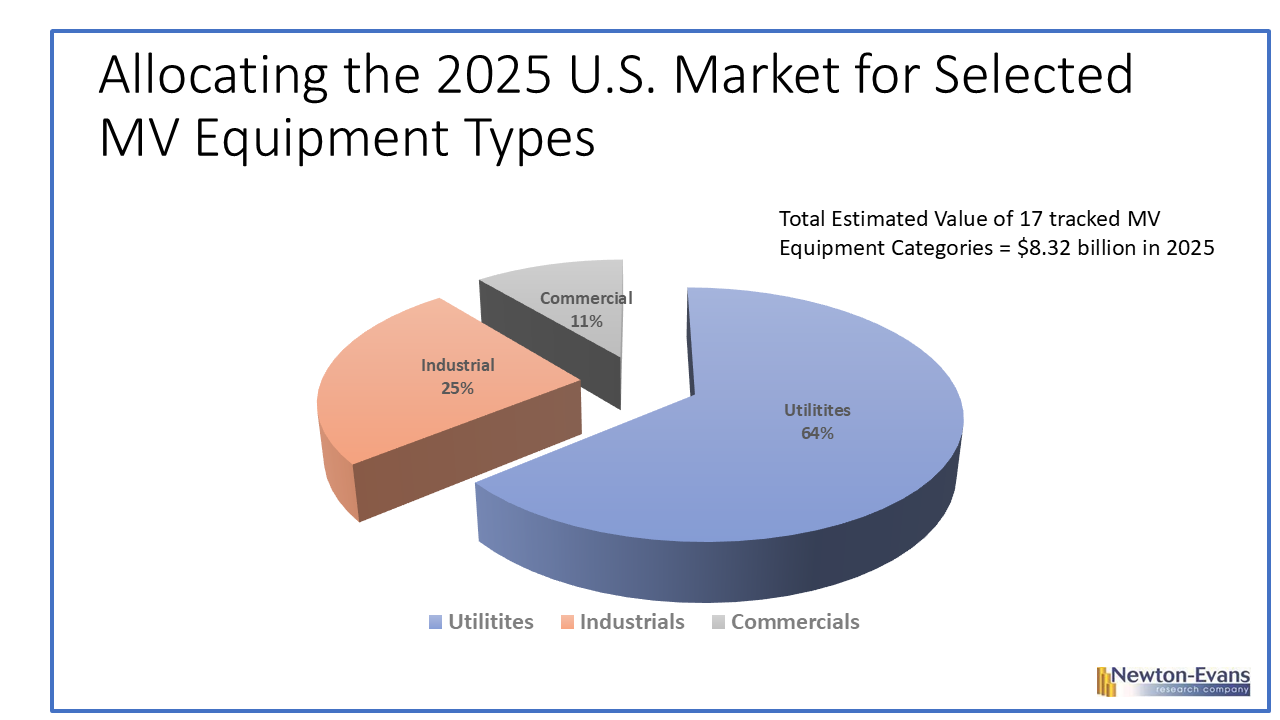

Importantly, commercial and industrial procurement of MV equipment have picked up substantially, in large part due to the rise of commercial developments including data centers and business campuses, and the re-shoring of multiple industrial facilities and the growth of utility-scale renewables facilities. The U.S. has added hundreds of new MV substations and added a few thousand distribution line miles as well since 2023.

The combined C&I segments purchase the majority of air-insulated metal-clad switchgear, MV gas-insulated switchgear, motor controllers, pad mounted switchgear, and comprise large shares of many other MV equipment categories. In total, Newton-Evans estimates that the C&I segment of the nation’s MV equipment market is now about 36% of the total and growing faster than the distribution utility segment. Industrial reshoring and plant expansions, along with large scale commercial developments, including data centers, are fueling this growth.

The commercial and industrial (C&I) segment of the T&D equipment and services market is currently growing as fast in many areas as is the utility market segment. Both segments are doing well for almost every category of equipment that is reported in the 2026-2028 edition of the MV Market Overview series. See Figure 1 below.

The C&I segment includes all non-utility owned power generation, transmission and distribution assets. Over the coming decade, more and more of the very large commercial and industrial sites are likely to become experienced owners/operators of power generation and T&D assets. Industry terms that have been around for decades including auto-generators and co-generators will again become widely associated with the developments of future data centers, commercial multi-site campuses and large industrial facilities. Utilities will be looked to for partnering, technical expertise, cooperative planning and perhaps joint purchase agreements for constructing and maintaining non-utility-owned G, T and D assets.

Topics covered in the 2026-2028 series of market overviews for MV equipment include individual report summaries covering major types of switchgear (air-insulated metal-clad, GIS, load interrupters, pad mount, submersible); reclosers and sectionalizers, outdoor circuit breakers, overhead disconnect switches, fused cutouts, substation class capacitors, instrument transformers, fault current limiters and Fault current indicators, current limiting fuses and fuse links and surge arresters.

At least two of these categories currently account for more than one billion dollars in domestic sales per year, while the value of shipments for five additional categories are more than $500 million in annual shipments to U.S. customers.

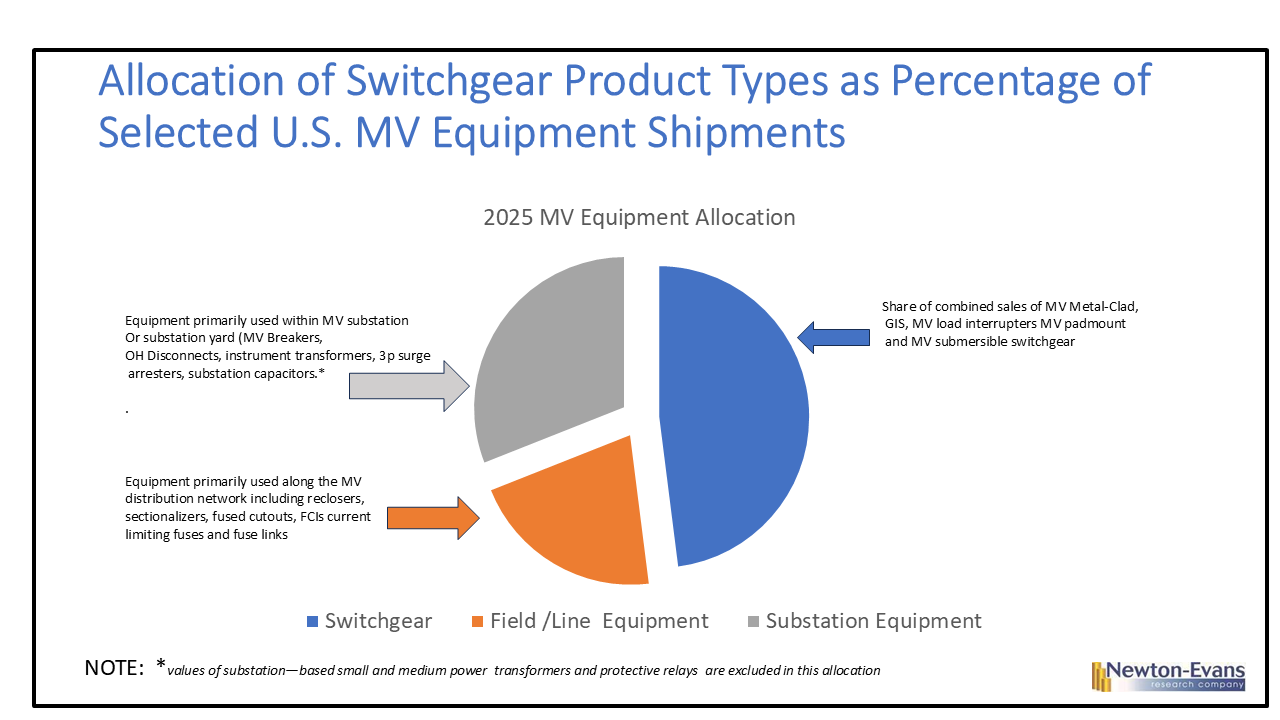

Combined revenue estimates for five types of MV switchgear account for just over one-half (53%) of the estimated value of all 17 equipment categories in the new report series. This assessment excludes the several hundred million dollars in shipments of overhead disconnect switches. See Figure 2 below.

Each of the 17 reports in the MV Market Overview series includes definitions of what is understood as the product segment, listings of key market participants and their estimated 2025 revenue, a market share assessment (pie chart), 2025 market size range estimates, and an outlook of estimated spending changes through 2028.

The data for these MV Market Overview reports has been obtained through secondary research, interviews with equipment/systems suppliers, industry consultants, the U.S. Department of Commerce, and from information gathered from more than 200 earlier Newton-Evans survey-based studies conducted through mid-2026.

summary reviews and highlights from completed studies

summary reviews and highlights from completed studies