As many long-term readers of Newton-Evans’ reports and articles knew from our assessment reported in 2009 there were back then three major contenders for the $7 billion Transmission and Distribution business units of the old Areva T&D Corporation. These were the American firm General Electric, the French corporate combination of Alstom and Schneider Electric, and the Japanese company, Toshiba. In the end the French government simply divided Areva T&D in half, and placed the “T” business into Alstom and the “D” business into Schneider Electric.

On June 21, 2014 GE was informed that Alstom’s board of directors decided to recommend GE’s offer to acquire the Power and Grid business of Alstom Corporation. These units are: Alstom Power (generation assets) and more importantly for this assessment, Alstom Grid, the HV and control systems components of the old Areva T&D business. The “D” business of Areva has now become a core business within the capable Schneider Electric camp of medium voltage equipment offerings.

Newton-Evans Research believes significant benefits to GE’s efforts targeting the global electric power industry will accrue if the company staffs truly work synergistically. Here are six key reasons for this view, in our opinion:

(1) IMPROVED WORLD MARKET ACCESS: GE will gain improved access to European electric power markets and other world regions with long-established relationships nurtured by Alstom and predecessors under the French management and government policies, which may continue under GE ownership, now that the French government is slated to become a significant shareholder investor in Alstom securities. Keep in mind that GE has more than a century of experience and accomplishments in France. I can recall visits to Belfort in eastern France and visiting both GE and Alstom (Areva) factory sites.

(2) ATTAINMENT OF ORGANIC GROWTH: GE Energy Management will again be able to lay claim to some real growth within 24 months of the close of this acquisition. Growth will come from both inorganic sources (via this acquisition – itself worth more than $4 Billion in current year sales of Alstom Grid products, systems and services) and organic growth (through increased interest in, and procurement of all combined GE-Alstom equipment, products and services). Each of the four component businesses of GE Energy Management including: Digital Energy, Industrial Solutions, Power Conversion and Energy Consulting will each benefit significantly if all goes as planned and envisioned in early July 2014. The big issue we see is whether Atlanta and Toronto will report in to Paris, or whether the reverse will be true.

(3) REDUCTION IN OFFERINGS “GAP”: GE will be able to fill several significant product/equipment gaps in its electric power transmission and distribution product line and related automation offerings. This will result in significant mid-term benefits to GE Digital Energy. However, a key issue for GE will be the “branding” of product offerings going forward from midyear 2015.

(4) MARKET-LEADING POSITION IN POWER GENERATION: Alstom’s power business includes assets for power generation such as turbines for coal, gas and nuclear power plants, wind farms while GE is a co-leader in both fossil, nuclear, hydro and renewables businesses.

(5) INCREASED SHARES OF OPERATIONAL CONTROL SYSTEMS: While GE’s EMS offerings have had somewhat limited success beyond North America, it’s DMS, OMS and GIS offerings are well-respected and are high quality offerings. Alstom Grid is a world leader in EMS, with a world-class group of systems for power transmission and distribution. The company’s “e-terra” line of systems is the leading market shareholder among critical T&D operational control systems used in the global electric power industry. The company also has developed a growing customer base among large utilities for advanced distribution network management with its IDMS offering. If the companies’ technical and product marketing teams work together as they have over time on various technical committees (IEEE, IEC, CIGRE et al) and provide smooth cross-systems integration capabilities, the company will be a force to be reckoned with in the world market for control systems. GE has a strong substation modernization/automation business focus across all components (systems, products, intelligent devices, communications equipment) that leads the North American market and is a growing force internationally.

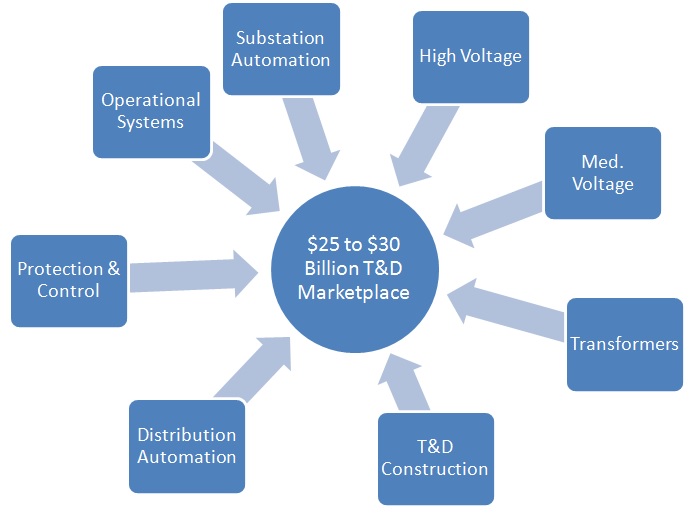

GE Energy Management will likely become a major player in several growing portions of the transmission equipment business, establishing a stronger foothold in the North American and international transmission market segments described below. Together these segments are worth $32-40 billion on a worldwide basis. Newton-Evans’ estimates that Alstom Grid earned about $3.5 billion to $4.1 billion in HV equipment sales in 2013.

Here is our take on the gains to be realized for both electric power infrastructure and electric utility automation and services:

FACTS and Reactive Power Compensation:

ABB is probably the global leader in flexible AC transmission systems and the related reactive power compensation segment of high voltage equipment for transmission networks. Siemens Energy is a strong number two supplier with several others (notably Mitsubishi Electric Power Products, and American Superconductor) also active in North America, and around the world. Alstom Grid and GE are also participants that together could challenge the market leading positions of ABB and Siemens within three years of a merger of product lines.

HVDC Equipment:

Siemens is the market leader in HVDC, with ABB a reasonably close second place share holder and MEPPI the likely third most important player. However, an integrated Alstom Grid-General Electric product grouping would enable the company to attain up to a quarter of the available market shares.

Gas Insulated Substations/Switchgear:

The North American market for High Voltage GIS equipment is in excess of a quarter billion dollars. While Alstom Grid has only a small share (stronger in Canada than in the US), GE Energy could now present itself as a player in this growing market segment of high voltage switchgear. GE would also play a much more important role in international markets where – unlike in North America – GIS equipment is prevalent. Globally, GIS equipment is a 2-3 billion dollar annual market.

High Voltage Bushings:

This relatively small (about $125-150M in annual worldwide sales) market is led by Siemens and ABB. However, the combined Alstom Grid and GE offerings could make GE into a formidable player in this segment.

High Voltage Capacitors:

GE Energy is already the major participant in the North American market for HV capacitors, but globally, ABB is the leader. Alstom Grid, by virtue of its recent acquisition of the Finnish manufacturer, Nokian Capacitors, is also a very strong player in Northern Europe. Together, the product lines could pose a real threat to ABB dominance here (yet another billion dollar global product segment).

High Voltage Circuit Breakers:

Alstom Grid is already a major player globally, and with GE’s “sales boots on the ground” could significantly increase its share in North America and abroad. ABB and Siemens are both very strong manufacturers in this large annual global market of better than $2 billion.

Disconnect Switches:

High voltage disconnect switches are vital components of many transmission systems, and the global market runs to about $500 million annually. GE and Alstom Grid are among the six leading suppliers of disconnect switches in North America, but lag behind Hubbell, S&C and Southern States, some of which offer circuit switchers used for disconnect applications.

Large Power Transformers:

Alstom Grid is number three in the world in terms of large power transformer market share and assets, operating 13 plants with an annual production capacity of more than 130 MVA. GE Prolec is a major North American market force with about a 14% share of the U.S. market. Together, this alliance may become number three in the global market for LPTs behind ABB and Siemens). To do so, the GE-Alstom combine will have to fend off HICO, Hyundai, Toshiba and MEPPI as well as three up-and-coming Chinese manufacturers.

Instrument Transformers:

The market for high voltage instrument transformers had been dominated by specialist “independent” manufacturers until recently. A recent buying spree had Siemens acquiring Trench Electric, Alstom Grid acquiring Ritz and ABB acquiring Kuhlman. Currently, the market for HV IT equipment is shared primarily by these three firms, with GE very active in the MV segment. Together, the combined HV/MV instrument transformer offerings of an integrated GE-Alstom Grid would change the shape of this market, which in North America alone hovers around $100 million, and close to one-half billion dollars worldwide.

Air Core Reactors:

Another component of some transmission network architectures, Siemens-Trench and Alstom Grid-Ritz are key players, with GE also strong and MEPPI further behind, but with a growing share. A number of smaller participants account for a rather large share of this $400 million global business.

Surge Arresters:

Another sizable market in its own right (about $1 billion per year globally) high voltage surge arresters are manufactured by a number of US-based firms such as Hubbell, Thomas & Betts, and Cooper Power, each of which competes quite successfully against the likes of ABB, Siemens and GE.

Automation Systems:

GE’s older XA/21 EMS platform and Alstom Grid’s highly rated E-Terra offerings are both held in high regard around the world, although GE’s systems are mainly installed in the USA. By year-end 2015 and more likely into 2016, General Electric-Alstom Grid will see benefits from world-leading combined market shares in substation automation, protection and control and T&D control systems (energy management, DMS, OMS, GIS and SCADA). Earlier (1990’s era) acquisition efforts have been fraught with initial business unit integration problems (to wit- ABB with its acquisition of the older Ferranti EMS business (Spider v. Ranger offerings) and Siemens-Control Data (Sinault-Spectrum v. Empros).

Substation Modernization:

If protective relays are included in the mix of substation modernization, then the collaborative efforts of GE and Alstom will lead to a global co-leadership market position across the board. Alstom Grid enjoys a strong position with transmission class relays and related MiCOM systems and equipment, and has been fairly strong participant in the global market for substation automation. GE enjoys a strong position in protective relays in North America (number two supplier) and in some Western European and Asian markets, and does make the list of qualified suppliers elsewhere.

Protection and Control:

Internationally, Alstom Grid (with part of the Stafford, UK-based relay business) holds an estimated 16% share of the global protective relay market (outside of the U.S.), estimated by Newton-Evans to be about $2.4-$2.6 billion this year. GE Multilin, based in Toronto, is also a very strong market participant, especially in the Americas, and is the leader in industrial protection and control markets.

T&D Services:

GE is a major participant in T&D equipment repair and services, especially with its transformer repair business, and Alstom Grid outside of North America earns about $550 million per year with its array of high voltage equipment services and global agreements for automation systems maintenance and upgrades.

Let’s not count this as a “done deal” quite yet. I do believe it is now very likely to be seen through by all parties (GE, Alstom, French government, possibly various international courts). The important role of Alstom’s minority shareholders and their reaction to the GE acquisition is somewhat unclear as is the role the French government’s strong minority ownership position will play. GE has made significant concessions regarding job retention among the French workforce, and has promised to add another 1000 jobs in the country. This could have ripple effects on its global workforce, especially if workforce reductions take place.

The following chart (used with permission of General Electric) illustrates the current state of the acquisition and the alliance formation.

summary reviews and highlights from completed studies

summary reviews and highlights from completed studies