Newton-Evans Research Company has completed hundreds of studies encompassing most aspects of the U.S. transmission and distribution equipment and related information management, monitoring and control systems markets in the nearly 36 years of its existence.

During the second quarter of 2014, the company will again be publishing more than 85 T&D segment management summaries which provide top-level overviews of most major components of T&D spending. These management summaries provide information on infrastructure topics as well as automation and control systems and engineering services. Definitions, Market size, market shares, recent year shipment estimates and the 2014-2016 outlook is provided in each summary. While some of the information provided in these reports is based on secondary research, much has been developed from meetings and discussions held directly with equipment manufacturers and systems integrators. In some instances, the supporting data is based on larger studies completed by Newton-Evans.

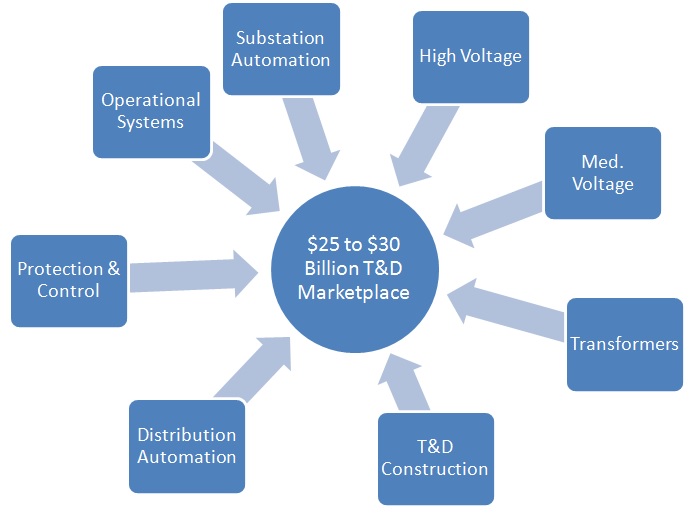

When coupled with the very large “third party services” market and operational communications network investments, T&D-related spending in the United States has grown to more than $25 Billion as of 2013. Importantly, much of these expenditures would occur naturally, without being classified as “smart grid” related. With a mature electrical infrastructure in place for decades, much of the procurement of T&D goods and services today centers on refurbishment and upgrades of existing facilities and field assets, and the smartening up of an older generation of “passive” equipment.

Spending for high voltage equipment itself accounts for more than $5 billion (excluding power transformers). HV substation upgrades, together with circuit breakers and switchgear, make up the bulk of HV-related spending. Gas insulated HV switchgear will likely grow in importance in the U.S. just as it has in countries around the world. Transmission monitoring and control is now being upgraded with the development and deployment of two relatively new technologies, synchrophasors and dynamic line rating systems. HV substation and transmission line/tower construction spending tends to vary each year and ranges from about $2.5 billion to more than $5 billion in recent years.

Shipments of medium voltage (MV) equipment are now approaching $4.5 billion in value. Major MV equipment categories include air-insulated metal-clad switchgear, reclosers and sectionalizers, load interrupters and surge arrestors. When coupled with spending for distribution automation, and a host of related services and control systems, MV-related spending exceeds $10 billion.

Looking at transformers, which can range from extra-large power transformers to medium power units, to a variety of pad-mount and pole-top distribution units, the value of product shipments for this entire category approaches $5 billion to about $6 billion in a “typical” year.

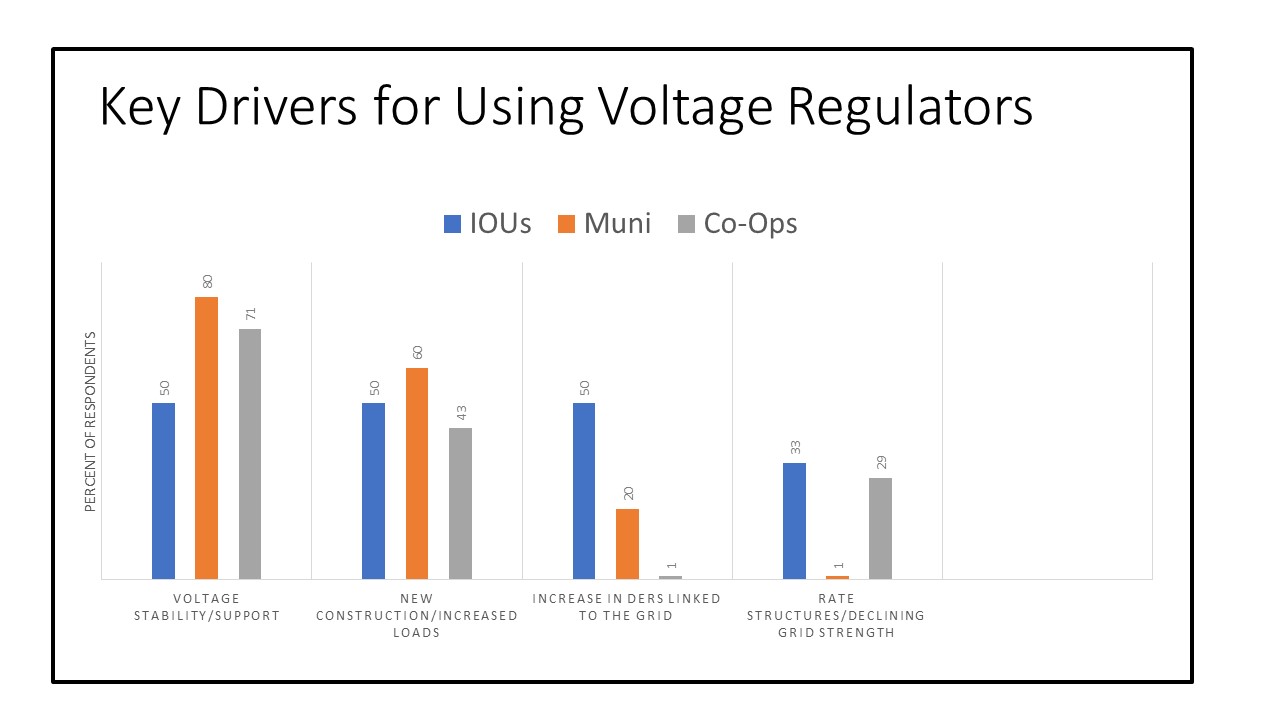

The emerging field of advanced distribution automation includes the monitoring and control systems supporting field instrumentation devices such as pole-top RTUs, faulted circuit indicators and controllers for capacitor banks and reclosers and voltage regulators. Supporting platforms required for processing data acquired from these devices include newer applications hosted locally, at substations or at the control center-based distribution management systems, which often includes modern “distribution SCADA” systems for mid-size utilities.

Operational control systems have been a mainstay of the electric power delivery industry since the early 1970s. Today, modern energy management systems are in operation in virtually every North American transmission utility. Distribution-focused SCADA systems are now installed and operating at nearly 1,900 U.S. utilities. Separate DMS hosting platforms supporting advanced DA activities are becoming prevalent in many of the largest utilities. When coupled with spending for geographic information systems, outage management systems, meter data management systems, mobile workforce management systems, market management systems, cyber-security applications software and supporting services, the annual external spending for supporting operational IT systems of the U.S. electric utility community is now approaching $2.5 billion.

Combining the very large market for systems protection in the form of protective relays, the market for smart/intelligent electronic devices (various types of substation meters, power quality monitors and event recorders) and the market for integration and processing of all of this data, the recent year aggregated market for HV and MV substation automation and modernization has hovered between $1.5 billion and $2 billion.

Realizing that the investor-owned community of electric utilities accounts for around 70% of all customers, industry revenues and spending on T&D, keep in mind that the 1,800 public power utilities and the more than 900 electrical cooperatives represent an attractive, growing (and often leading edge) user base for newer technologies, especially for MV equipment, systems and services.

In addition to the electric utility community, the 710,000 industrial companies and nearly 18 million commercial firms account for about 15% of all T&D equipment and services purchased in this huge $22-$25 billion marketplace.

Unlike many countries around the world, and unlike many other components of the American economy, U.S.-based factories produce more than 90% of all T&D equipment purchased by U.S. utilities. A few years ago this was not the case for large power transformers, but with the opening of several manufacturing facilities in the southern U.S., this has changed for the better, and has resulted in shortened lead times for power transformers. North American-based business operations also develop and provide the vast majority of services, systems and applications software needed for utility operations and implement virtually all control and monitoring systems used here.

In multiple recent studies conducted by Newton-Evans, the nation’s electrical equipment manufacturers have reported that they have the capabilities to produce whatever may be required to advance the development of a more resilient, more reliable power grid. Smaller firms continue to lead in research and development of advanced energy technologies, and the follow-on benefits of the 2009-2012 ARRA programs under the guidance of the U.S. Department of Energy continue to positively impact the development of a 21st century electric grid.

It will take sustained investment over the next 20-30 years, along with ongoing research and development, to realize a fully reliant, resilient and sustainable power grid here and elsewhere. The development of demand response techniques, inclusion of distributed energy resources, deployment of micro—grids, large scale energy storage, cost-effective underground distribution networks where sensible, and the integration of renewables are each poised to play an important role in the future development of a modern American grid. We don’t need to tear down and start over, but we do need to modernize and upgrade the grid components in an iterative and intelligent manner. We need to improve and safeguard what remains as one of the world’s great technical achievements of the past century, the North American electric power grid.

summary reviews and highlights from completed studies

summary reviews and highlights from completed studies