For October’s and November’s lead articles, we have developed overviews describing electric utility-related control systems on the OT side and in December will cover key administrative and business management systems from the IT side. This month’s lead article discusses the various aspects of energy management systems, supervisory control and data acquisition systems, and advanced distribution management systems.

Before a discussion of these three control systems begins, we must acknowledge the brave new world of OT being re- shaped and updated by the inclusion of artificial intelligence (AI) and machine learning (ML) in each of these control systems types. By late 2022, we began to see artificial intelligence playing a role in the project development side of major EMS, SCADA and ADMS suppliers. By 2025, commercial adaptation of AI has become widespread among energy systems suppliers for several critical applications, including improved load forecasting, dynamic load balancing, improving renewables integration efforts, and related areas including energy storage.

AI is enabling smarter, more efficient, and more sustainable electric power usage. AI’s ability to analyze vast data sets and identify complex patterns helps to optimize every stage, from energy generation and distribution to consumption. Over the coming years, AI will be integrated into more aspects of grid management and grid operations, improving reliability, safety and security for the world’s grid operators, large and small. Across the U.S., Ai will also play a pivotal role for ISOs and RTOs, as they continue to deal with integration requirements of non-utility participation in the transmission market.

An Energy Management System (EMS) is a suite of generation and transmission applications software tools used to monitor, control, and optimize the performance of generation and transmission systems designed to reduce energy consumption, improve the utilization of the system, increase reliability, and predict electrical system performance as well as optimize energy usage to reduce cost.

By 2019 vendors were taking note from the term ADMS and began using the term AEMS to indicate significant new capabilities including the integration of renewables and energy storage and their impact on grid operations and voltage stability. Coupled with the rapidly increased speed of processing and analyzing contingencies, and the ability to dispatch and curtail distributed energy resources, these developments have helped enhance operator capabilities and visibility into the real-time electric network. As the power generation mix and transmission requirements have become more complex, AEMS developments and capabilities are keeping pace with such needs. More recently, new iterations of generation management systems (GMS) have been developed that now include many of the generation-side applications that were (and continue to be) components of an EMS as described in our report on GMS (OT/IT11).

Three major components of a modern EMS include:

- Native Services: data acquisition and control; graphical user interface; linkage/connectivity options to other systems; large database capabilities. There are many objectives of an energy management software including an application to maintain the frequency of a Power Distribution System and to keep tie-line power close to the scheduled values.

- SCADA Services: load shedding, load restoration, network status; sequential control, switch order management, playback of historical events

- Advanced Power Systems Applications (or Network Application Services): to include generation dispatching and control [AGC], transmission security management; voltage transient stability; unit commitment; state estimation, contingency analysis, demand forecast, and dispatcher training simulator. Added to these improved capabilities from earlier generations of EMS, are the abilities to work closely with and to better manage the influx of distributed energy resources and energy storage installations, the bulk of which may not be owned or operated directly by the utility. Finally, the adoption of the Common Information Model (CIM) across the industry has been a helpful development.

Sources: GE Digital Energy, ETAP, Hitachi Energy, OSII, PSC Consulting, Siemens Energy, Schneider Electric.

Among the benefits of modern EMS installations are the enhanced decision-making on the part of system operators enabled with AI. The role of digital twins will enable a more real-life training environment for new operators, as the newest iteration of simulation systems. Overall operational efficiency will be improved, providing greater grid stability, earlier detection of system anomalies, reduction in outage downtime and improved system safety for all.

Supervisory Control and Data Acquisition (SCADA) is a type of industrial control system (ICS). Industrial control systems are computer-controlled systems that monitor and control industrial processes that exist in the physical world. SCADA systems historically distinguish themselves from other ICS systems by being comprised of large-scale processes that can include multiple sites, and large distances. In addition, electric power distribution SCADA remains a more-or-less “open loop” type of control system, with human operators monitoring and supervising the actions of the control computer as it acquires data continuously from power substations and other remote locations, including third party operated distributed energy resource sites in an electric utility network, now marking more than 4,000 distinct utility-scale generation sites across the U.S.

Newton-Evans believes that there is a significant opportunity for providers of SCADA-related systems and application software to help manage the operations of commercially-owned utility-scale wind and solar power resources, as SCADA systems become more capable, adaptive, and scalable. By doing so, there will be somewhat of a more “closed loop” look-and-feel, but human operators will continue to play an important role and adapt to changing distribution network environments.

For more information on renewables SCADA opportunities, see https://www.newton- evans.com/scada-systems-for-the-renewables-energy-industry-and-adms-for-utilities/

Advanced Distribution Management Systems (ADMS) and Advanced Distribution Automation are terms used to describe the extension of intelligent control over electrical power grid functions to the distribution level and beyond. It is related to distribution automation that can be enabled via the smart grid. If we were to include all the possible components of a comprehensive ADMS, the U.S. market value would exceed $1 Billion. In this report, we are attempting to isolate ADMS core functions in a separate manner and retain individual product categories or sub-markets for OMS, GIS, WFMS, GMD, DERMS and others.

Typically, electric utilities with energy management systems have extensive control over transmission-level equipment, while Distribution SCADA offers increasing control over distribution-level substation-based data acquisition equipment (RTUs, PLCs and/or platforms and gateways). ADMS implementations provide additional utility operator monitoring and control capabilities over smart components in the distribution network beyond the substation using primarily wireless communications. In many ADMS installations, the same platforms are used, with additional applications implemented to provide coordination and control of automated field devices.

Gartner has defined an ADMS similarly, as follows: An advanced distribution management system (ADMS) is the software platform that supports the full suite of distribution management and optimization. An ADMS includes functions that automate outage restoration and optimize the performance of the distribution grid. ADMS functions being developed for electric utilities include fault location, isolation and restoration; volt/volt-ampere reactive optimization; conservation through voltage reduction; peak demand management; and support for microgrids and electric vehicles. https://www.gartner.com/en/information-technology/glossary/advanced-distribution-management-systems-adms

West Monroe further defines ADMS as: The ideology of an ADMS is simple—a modular system with an OMS, DMS, and Distribution SCADA (D-SCADA) at its core (as depicted in Figure 1).

However, we found that utilities and vendors use the term differently. To a utility, an ADMS is the aggregate system (at least one module addition to an OMS) to manage outages and operate the distribution system in a safe and efficient manner. https://www.westmonroe.com/perspectives/resource/advanced-distribution-management-systems-adms-the-core-of-the-utility-of-the-future

The U.S. Department of Energy’s NREL has also provided a detailed roadmap for ADMS and states on its website:

The “advanced” elements of an ADMS go beyond traditional distribution management systems by providing next-generation control capabilities. These capabilities include the management of high penetrations of distributed energy resources (DERs), closed-loop interactions with building management systems, and tighter integration with utility tools for meter data management systems, asset data, and billing. https://www.nrel.gov/grid/advanced-distribution-management.html

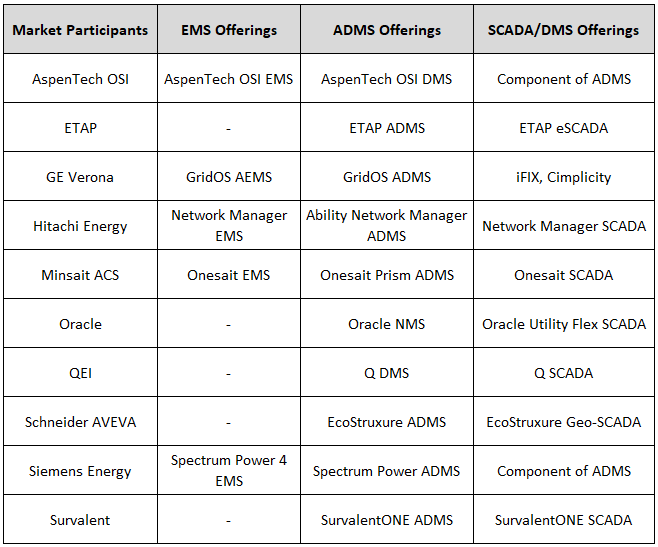

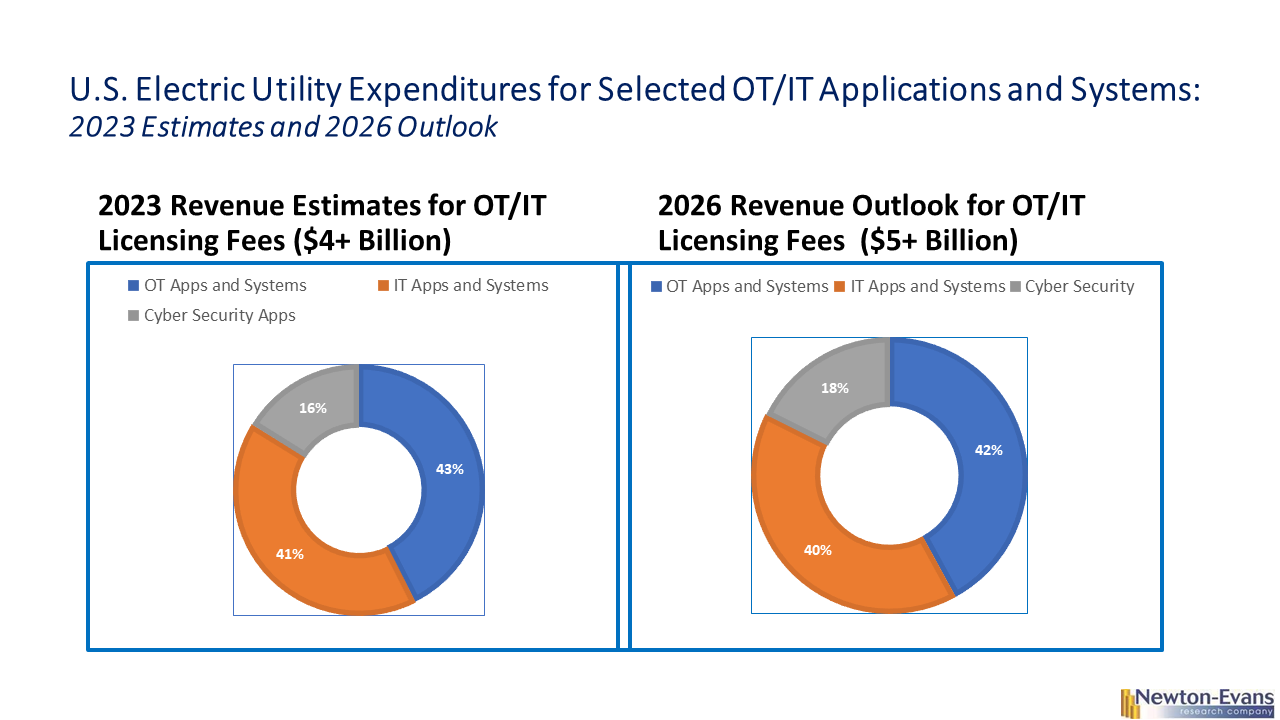

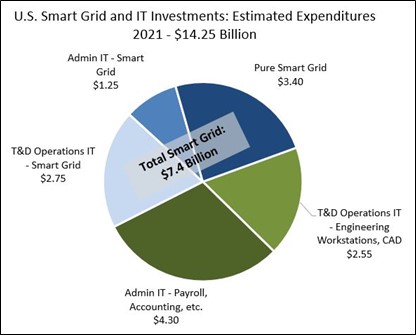

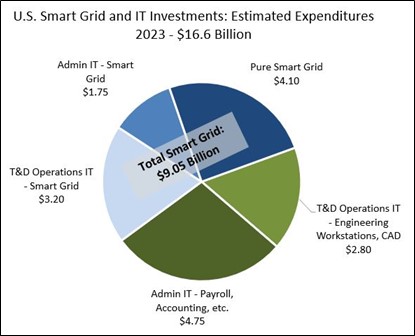

U.S. market size estimates, shares and outlook for each system type are reported in the OT/IT Market Overview Series of 12 topical Newton-Evans’ reports.

summary reviews and highlights from completed studies

summary reviews and highlights from completed studies